Prop firms that expanded from forex into crypto spot, perpetual futures, indices, and commodities are discovering that their liquidity stacks — wired for a single asset class — cannot keep pace with the operational and technical demands of a genuinely multi-asset operation.

Who this is for: Prop trading firm operators, brokerage CTOs, and liquidity infrastructure decision-makers navigating the shift to multi-asset operations.

In three points, you will learn:

- Why “adding instruments” at a prop firm triggers a cascade of infrastructure changes — not just a symbol list update

- How crypto perpetual futures introduce a data and margin model that legacy FX infrastructure was never designed to handle

- What a purpose-built, crypto-native liquidity connectivity layer looks like in practice, versus a forex hub with crypto bolted on

The Drift from Forex — And the Numbers Behind It

The prop trading industry was born, structurally speaking, in the forex market. Evaluation challenges were priced in pips. Risk parameters were built around currency pair volatility profiles. The liquidity models underneath assumed that traders would operate in deep, 24/5 markets with familiar instruments, well-understood LP relationships, and a reasonably predictable flow of institutional price formation.

That world still exists. But it is no longer the whole picture.

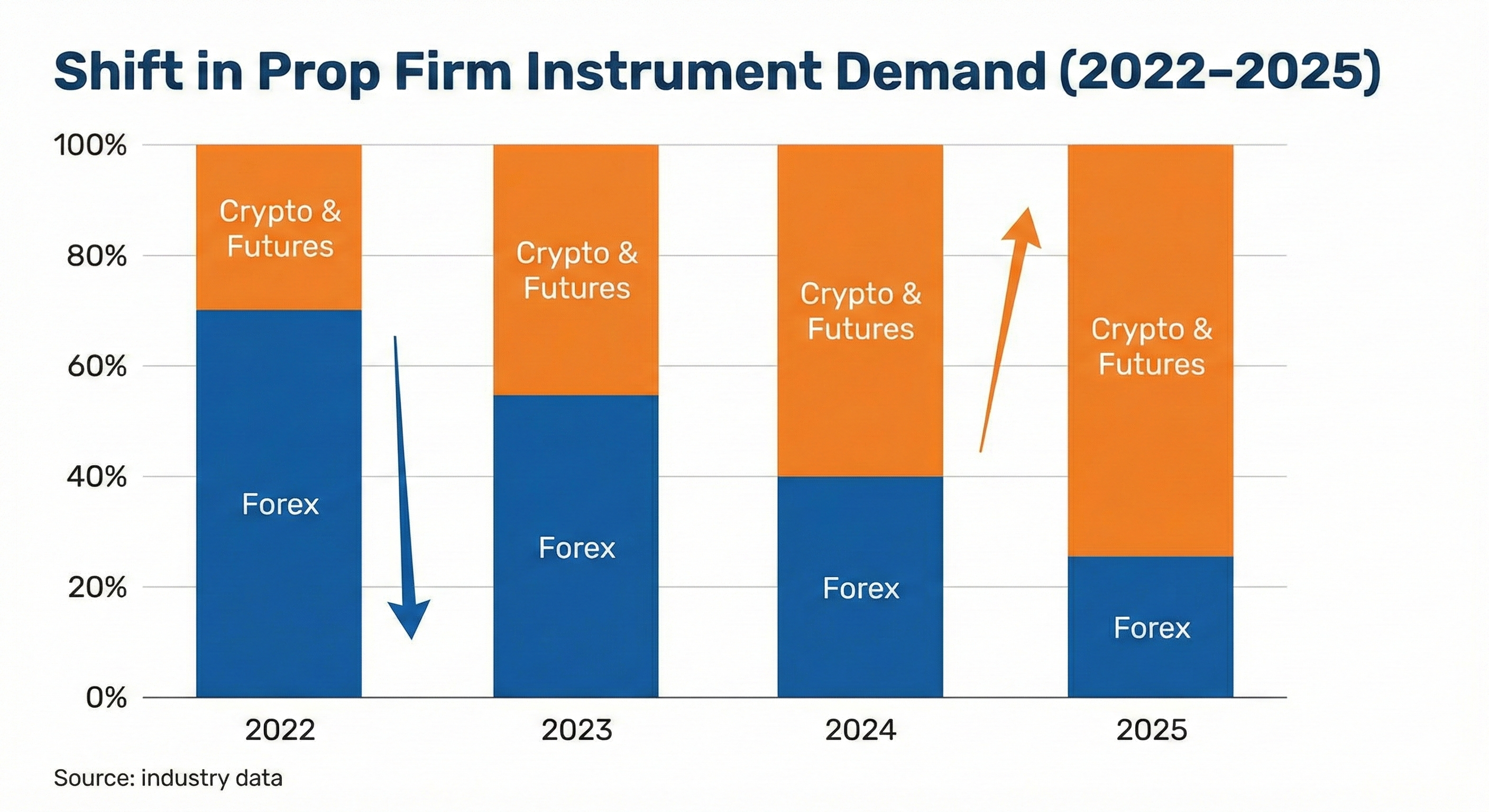

By late 2025, something significant had shifted in the search and activity data from the prop trading sector: interest in futures-based prop trading overtook forex for the first time. FTMO added 22 new cryptocurrency trading pairs in July 2025 — including SOL, BNB, XLM, AAVE, and LINK — signalling that the market’s largest prop operator by account volume was responding to explicit demand, not experimenting. The Trading Pit, now operational in over 180 countries with more than 450,000 trades processed monthly, was named “Best Multi-Asset Prop Trading Firm 2025” at the FundedTrading Awards. Blue Guardian launched a dedicated CME futures division in 2025. FundedNext, The5ers, and a wave of challengers have entered or announced entry into futures, crypto derivatives, and indices products.

The commercial rationale is not hard to understand. Younger cohorts of traders — the demographic engine of the prop sector’s 1,264% expansion since 2015 — arrived in markets through crypto and video game-inflected mental models. They expect 24/7 access. They are comfortable with leverage expressed as a funding rate rather than a margin ratio. They want to trade BTC/ETH perpetuals on the same platform where they hold a funded forex account, and they will route to whichever firm delivers that experience most cleanly.

The problem is that the liquidity infrastructure powering most of these firms was not designed for what they are now trying to do.

What “Multi-Asset” Actually Means for the Liquidity Stack

There is a tendency to think of adding a new asset class as a product decision: flip a setting, configure a symbol list, apply a spread markup, and you are live. In practice, each asset class a prop firm adds does not extend an existing system — it introduces a new sub-system, each with its own operating assumptions.

Consider the gap between the instruments a typical multi-asset prop firm now advertises:

Forex majors and minors: Five-decimal pricing, continuous weekday sessions, deep interbank liquidity sourced via Prime of Prime relationships, well-established A/B-book risk models, swap rates calculated from overnight interest differentials.

Crypto spot: 24/7 trading with no settlement netting at end-of-day, counterparty relationships with centralized exchanges rather than banks, mark-to-market liquidity that can compress dramatically in seconds, and pricing feeds that diverge materially across venues during volatility events.

Crypto perpetual futures: All the characteristics of crypto spot, plus a funding rate mechanism — typically settled every 8 hours — that creates a continuous cash flow between long and short position holders. The price of a perpetual is anchored to spot via this mechanism, but the anchor can stretch violently.

Indices (US equity, global equity): Exchange-traded derivatives with defined session hours, overnight gap risk, margin models derived from underlying equity market conventions, and settlement structures entirely unlike either FX or crypto.

Commodities (energy, metals, agriculture): Storage costs expressed as roll yield, contango and backwardation dynamics that affect the economics of holding positions, delivery specifications that have to be handled contractually even if never exercised.

None of these operate on the same clock, the same margin logic, or the same LP relationship structure. The infrastructure layer that connects a prop firm to liquidity — the bridge, the price construction engine, the risk management module, the execution routing system — needs to be able to hold all of these models simultaneously without forcing them into a single, simplifying assumption that was calibrated for forex.

When legacy forex infrastructure is extended to handle crypto, what typically happens is that crypto spot gets mapped onto a forex-style model: spread markup applied, B-book for challenge-phase simulation, and perhaps a limited A-book hedge to an exchange for funded traders. That works, at the margin, for BTC/USD and ETH/USD spot. It begins to break for altcoins, where liquidity is materially thinner and exchange-to-exchange pricing divergence is wider. And it does not work at all for perpetual futures — for reasons that deserve their own section.

The Perpetual Futures Dimension: Where Legacy Infrastructure Breaks Down

Perpetual futures now represent approximately 75% of all crypto derivatives trading volume globally, according to analysis from TD Securities published in November 2025. That is not an asset class that sits at the edge of the crypto market — it is the crypto market’s primary form of price formation for leveraged positions.

Understanding why perpetuals are infrastructurally distinct from every other instrument requires briefly understanding the funding rate mechanism. A perpetual futures contract has no expiry date. To prevent the contract price from drifting permanently away from the spot price, exchanges impose periodic funding payments — typically every 8 hours — between long and short holders. When the perpetual trades above spot (positive funding), longs pay shorts. When it trades below (negative funding), shorts pay longs. The magnitude of these payments reflects market sentiment and positioning.

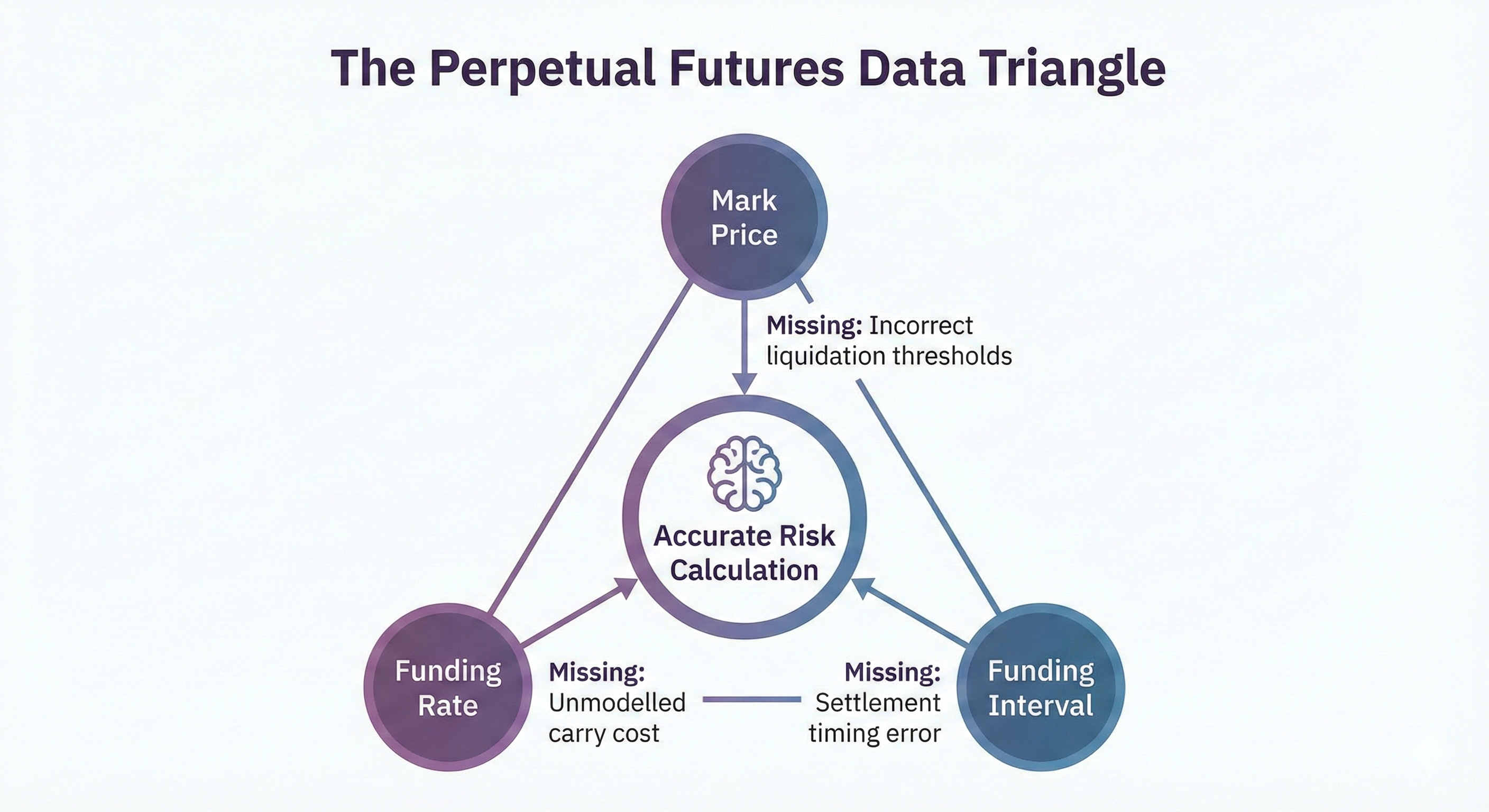

For a liquidity hub or bridge connecting prop firms to this market, there are at least three data dimensions that do not exist in any TradFi instrument:

- Mark price: The reference price used for unrealized P&L and liquidation calculations. In perpetuals, mark price is not simply the last trade price — it is typically a weighted index derived from spot prices across multiple exchanges, adjusted to smooth manipulation risk.

- Funding rate: The current applicable rate, which varies continuously and must be streamed in real time to allow traders to model the cost of holding positions.

- Funding interval: The periodic schedule on which funding settles, which varies by exchange and sometimes by instrument.

A risk engine that is not receiving and processing these three fields in real time cannot accurately model the exposure of a funded trader’s perpetuals book. It cannot correctly calculate the economic cost of overnight holds. It cannot accurately determine whether a trader is approaching their drawdown limit because it is missing a material component of their position’s carrying cost.

This is not a theoretical gap. In the October 2025 market dislocations, risk infrastructure that relied on last-trade pricing rather than mark price calculations showed material errors in real-time exposure estimates. Prop firms whose bridges were transmitting only top-of-book quotes from a single exchange found themselves unable to accurately determine their funded traders’ P&L positions in real time.

The infrastructure bar for perpetuals is simply higher. And the prop firms expanding into this space are discovering that not all connectivity layers are built to meet it.

Synthetic Instruments as a Bridge — and Their Limits

One mechanism that sophisticated liquidity infrastructure provides to manage the gap between what a trader wants to access and what is directly available via a single LP is the synthetic instrument engine.

A synthetic instrument combines two or more underlying assets, contracts, or financial instruments to achieve a specific exposure. In practice, this might mean constructing a BTC/EUR price feed by combining BTC/USD and EUR/USD pricing from different providers; or synthesizing an altcoin pair that no single LP quotes by routing through a common intermediate. For prop firms, the ability to offer a broader instrument catalogue without requiring direct LP relationships for every symbol is commercially meaningful.

But synthetic construction introduces its own infrastructure requirements. The engine must receive source feeds from both components with sufficient reliability and at sufficient frequency to construct a synthetic quote that does not introduce its own pricing anomalies. Invalidation logic — the mechanism that removes a synthetic quote from the book when one of its component feeds becomes unreliable — must apply consistently across organic and synthetic symbols alike. A client that receives a stale synthetic price because one component’s feed timed out but invalidation was not triggered has worse execution than a client with no access to that pair at all.

The operational conclusion here is that synthetic instruments extend the liquidity stack’s reach — but they do not reduce the underlying requirement for robust, low-latency connections to multiple, high-quality liquidity sources across multiple asset classes.

The LP Diversity Problem: One Asset Class, One Relationship Is No Longer Enough

A forex prop firm operating in a single-LP or even dual-LP structure can function. The relationship is well-understood: the PoP provides aggregated interbank pricing, the firm applies markup, and risk is managed through a combination of internalization and external hedging. The LP universe is relatively consistent: the same counterparties cover most of the major currency pairs.

The moment a prop firm adds crypto spot and perpetuals to its product set, that model breaks. Crypto spot liquidity is sourced primarily from centralized exchanges — Binance, Bybit, Kraken, Coinbase, Crypto.com, HTX — each with different API characteristics, different depth profiles by trading pair, and different latency properties. Perpetuals liquidity is concentrated further: Binance and Bybit together dominate a substantial share of global perp open interest, but the specific depth for any given altcoin perpetual can vary significantly between them, and the mark price calculations differ between venues.

This means the liquidity stack servicing a multi-asset prop firm must maintain live, stable, low-latency connections to a portfolio of crypto exchange integrations simultaneously. It must handle the specific characteristics of each exchange’s API — for example, Binance Futures’ WebSocket API (adopted for its 4x improvement in average round-trip time) versus a REST-based fallback — and it must manage reconnection logic, IP rate limits, and duplicate execution report handling robustly enough that a momentary exchange-side disruption does not cascade into the prop firm’s risk or position tracking systems.

The operational reality of managing this portfolio of exchange relationships — credential management, API key rotation, rate limiter compliance, connectivity monitoring with fast failover detection — is non-trivial infrastructure work. It is not work that a prop firm’s dealing desk should be doing in-house. It is the function of a purpose-built liquidity connectivity layer.

Execution Model Complexity: Challenge Phase vs. Live Routing Is Not the Same Problem

The execution model architecture for multi-asset prop firms is more nuanced than for traditional retail brokerages, and the nuance scales with the number of asset classes being offered.

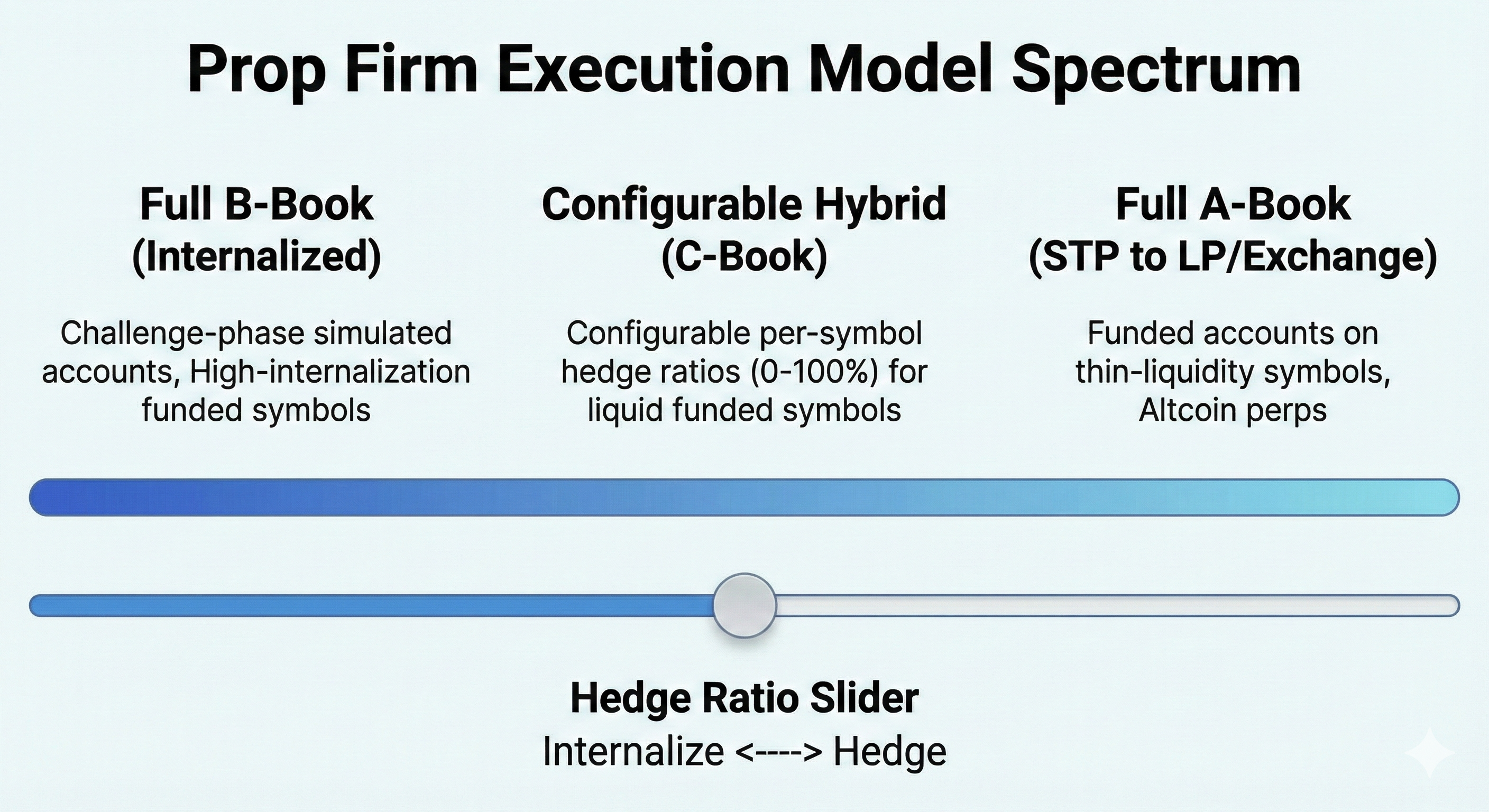

During the challenge phase — when a trader is operating on a simulated account, and the prop firm’s revenue derives primarily from evaluation fees — the firm typically internalizes all trades. There is no external hedge. The position risk is virtual. The infrastructure requirement is for accurate price simulation: the challenge environment must reflect real market conditions closely enough to be a valid test of trading skill, which means real-time pricing feeds from the actual LP stack.

Once a trader passes and moves to a funded account, the calculus changes. Now the firm carries real P&L exposure on the funded account’s positions. The question of how much of that exposure to hedge externally, versus internalize and manage in aggregate across the funded trader pool, becomes commercially significant.

A hybrid execution model — sometimes called a C-book or configurable-hedge approach — allows the firm to set per-symbol hedge ratios. For highly liquid instruments like BTC/USD spot, where the firm can absorb significant internal flow and offset it through netting across multiple funded traders, a low external hedge ratio may be appropriate. For a thin altcoin perpetual where internalization creates concentrated directional exposure, a higher external hedge ratio — routing more of the flow to the exchange — makes more sense.

The challenge and the funded phase are not the same engineering problem. A prop firm that conflates them — running funded traders on the same fully-internalized infrastructure designed for challenges — will eventually discover that the exposure profile of a successful, skilled trader bears little resemblance to the exposure profile of a random evaluation entrant.

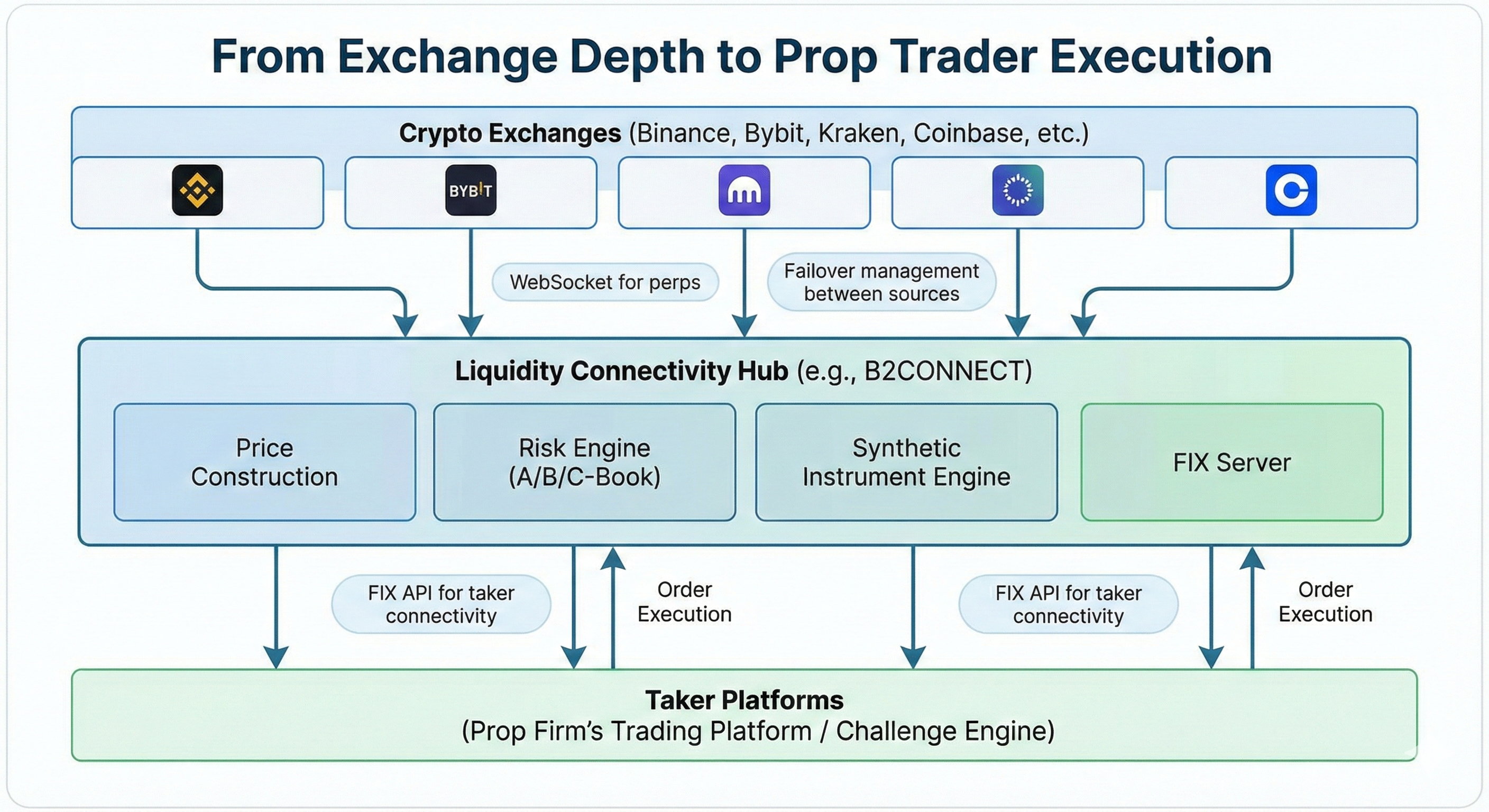

Architecture Snapshot: What a Multi-Asset Prop Firm’s Liquidity Stack Actually Looks Like

Stepping back from the individual components, it is useful to think about the liquidity stack for a mature multi-asset prop firm as a sequence of distinct functions, each with specific technical requirements.

Layer 1: Exchange Connectivity — Direct API connections to the centralized exchanges providing liquidity for crypto spot and perpetuals. Each connection must handle the exchange’s specific authentication, rate limiting, and message protocol (REST, WebSocket, FIX where available). Failover management ensures that if a primary source becomes unavailable, routing switches to a backup without disrupting active price feeds or order management. For perpetuals specifically, this layer must transmit mark price, current funding rate, and funding interval alongside top-of-book and depth quotes.

Layer 2: Price Construction and Normalization — Received quotes are normalized across exchanges (different tick sizes, decimal precision, and timestamp formats) and assembled into a coherent price feed for each instrument. Markup is applied at this layer. Synthetic instruments are constructed here by combining normalized component feeds. Negative spread filtering prevents anomalous quotes from propagating downstream.

Layer 3: Risk Engine — The risk engine receives the normalized price feed and all open positions from the connected prop firm’s trading platform. It applies the configured execution model (A/B/C-book, hedge ratios per symbol), monitors NOP (Net Open Position) exposure, tracks unrealized P&L against funded account drawdown limits in real time, and triggers hedging activity when configured thresholds are reached. For perpetuals, it must incorporate funding rate accruals into P&L calculations.

Layer 4: Taker Connectivity — The prop firm’s trading platform connects to the liquidity hub as a “Taker” via FIX API or WebSocket, receiving market data and sending orders. The FIX server must handle subscribe/unsubscribe cycles robustly, including from third-party aggregators that may not fully adhere to FIX standards.

Layer 5: Monitoring and Reporting — Real-time monitoring of connection state, order statistics, and quoting quality per LP. Execution reporting and trade capture for audit, risk review, and regulatory purposes. Notification routing for operational events (LP disconnections, anomalous spreads, threshold breaches).

This is the architecture that a crypto-native liquidity hub provides. It is not a forex bridge with a crypto adapter appended. It is a stack where every layer was designed from the outset with the specific requirements of centralized exchange connectivity and crypto derivatives in mind — and which has subsequently proved applicable to the multi-asset TradFi instruments that prop firms are now adding alongside.

FAQ

What makes a crypto-native liquidity hub different from a traditional forex Prime of Prime?

Why does the funding rate matter to a prop firm’s risk department?

Can a prop firm add crypto to its platform by routing through a single exchange?

What is a synthetic instrument in the context of a multi-asset liquidity hub?

What does “configurable hedge ratio per symbol” mean in practice?

How does FIX API connectivity work for prop platform integrations?

Is a liquidity hub deployment for a prop firm a self-service or managed process?

Key Takeaways

- Multi-asset expansion is the commercial direction of travel for prop firms in 2026, driven by trader demand for crypto, futures, and indices alongside forex — and the infrastructure implications are non-linear.

- Each asset class a prop firm adds introduces a new sub-system with distinct LP relationships, margin models, session logic, and data requirements — particularly for crypto perpetual futures.

- Perpetual futures require transmission of mark price, funding rate, and funding interval alongside standard price data. Liquidity infrastructure that does not provide these fields cannot accurately model a funded trader's real-time P&L or drawdown position on perps.

- Synthetic instrument construction extends the accessible instrument catalogue — but it is not a substitute for reliable, multi-LP connectivity, and the quality of a synthetic depends entirely on the quality of its component feeds.

- A configurable per-symbol execution model (A/B/C-book with adjustable hedge ratios) is the right architecture for multi-asset prop operations, because the optimal internalization ratio differs materially between liquid crypto majors and thin altcoin perpetuals.

- The shift to multi-asset prop trading requires a liquidity connectivity layer that was designed for the complexity it now has to manage — not one that was extended from a simpler, single-asset-class starting point.

If you are building or scaling a multi-asset prop trading operation and want to evaluate liquidity connectivity infrastructure that was designed for this complexity from the ground up, speak to the B2CONNECT team.

Sources and references

Finance Magnates, “Retail Trading & Prop Firms in 2025: Five Defining Trends,” December 2025. · TD Securities, “Perpetual Futures: The Missing Link in Tokenized Equities,” November 2025. · QuantVPS, “Top Multi-Asset Prop Trading Firms,” January 2026. · FTI Consulting, “Crypto Crash Oct 2025: Leverage Meets Liquidity,” December 2025. · AlphaPoint, “Perpetual Futures in 2025,” August 2025. · B2BROKER, “B2CONNECT Update: More Integrations, Broader Connections,” April 2025. · B2BROKER, “B2CONNECT Update: Enhanced Liquidity & FIX Protocol,” June 2025. · Atmos by Taurex / Prop Firm App, “Prop Firm Statistics 2026,” January 2026. · BestPropFirms, “Prop Trading Statistics 2025.” · For Traders, “Why Prop Firms Are Booming in 2025.” · Bitrates, “Top 3 Prop Trading Firms for Crypto Traders in 2026,” January 2026.

Reviewed by the B2CONNECT Product Team · February 2026

Further reading: B2CONNECT FIX API documentation · B2CONNECT Release Notes